Here’s a practical guide to using the “Profit First” accounting model in your law firm to create stability, reduce stress — and build a business that pays you first.

Table of contents

- Why Law Firms Struggle Financially — Even with Good Revenue

- Profit-First Accounting, Explained Simply

- The Five Profit First Accounts

- Implementing Profit First Without Disrupting Your Entire Practice

- What This Reveals About Your Pricing and Spending

- A Quick Word About Trust Accounts

- Don’t Let Profit Be a Dirty Word

- A Few Pitfalls and How to Avoid Them

- What Changes When You Prioritize Profit

- More Money Management Tips for Law Firm Owners

For solo and small firm attorneys, the pressure to bill more, spend carefully and still end the year with a healthy bottom line never really goes away. The problem isn’t always revenue — it’s how that revenue gets used. Many firms follow the traditional flow: bring in money, pay the bills, and hope there’s something left. The “Profit First” accounting model, first introduced by Mike Michalowicz, flips that logic.

Instead of treating profit as a leftover, the Profit-First accounting method treats profit as the first priority, and forces the law firm business to operate within healthier boundaries as a result.

Profit doesn’t show up by accident. It happens when the business is built to produce it from day one. Profit First gives law firm owners a simple way to stop chasing margins and start claiming them — with a system that makes profit automatic, not occasional.

Why Law Firms Struggle Financially — Even with Good Revenue

A solo attorney can bring in $500,000 a year and still feel like they’re barely scraping by. It’s not just about how much you earn. It’s how that money gets handled from the moment it enters your operating account.

Here’s where law firms run into trouble:

The money always seems to go somewhere. It’s easy to assume you’ll make enough to cover everything, but without a system in place, expenses expand to match income. More revenue doesn’t create more margin — it creates more ways to spend.

Owner pay is inconsistent. Many attorneys pay themselves last, waiting until all expenses are covered and hoping there’s enough left for them. That makes personal income unpredictable, and usually the first thing cut during a slow month.

Read: “Building a Law Firm That Pays You First: The Rule of Thirds” by Brooke Lively

Taxes become a source of stress. Without a designated place to set aside tax money, firms can end up scrambling to cover quarterly payments. Even with decent revenue, the lack of a clear tax reserve creates last-minute pressure and disrupts cash flow.

Profit-First Accounting, Explained Simply

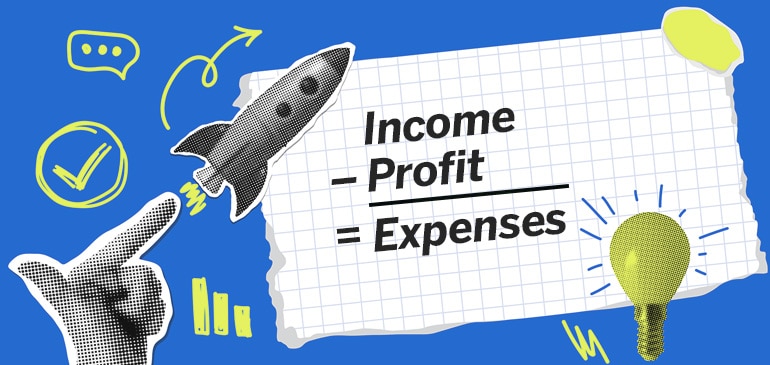

The core of Profit First is straightforward:

Revenue – Profit = Expenses

In practice, that means you take a percentage of every dollar that comes in and immediately set it aside as profit. What’s left is what you run the business on.

To make it work, you use multiple banking accounts, each with its own specific job.

The structure makes your cash easier to manage by assigning every dollar a job as soon as it hits your account.

The Five Profit First Accounts

You don’t need a finance background to implement Profit First. You just need to open a few accounts and set up a habit of moving money between them on a consistent schedule.

1. Income Account. The income account is the holding tank. All payments land here first. Nothing gets paid directly from this account — its only job is to receive money before it’s distributed.

2. Profit Account. Take a percentage of every deposit and move it here. You don’t touch it. You don’t borrow from it. The profit account is your quarterly reward as a business owner — or your emergency cushion if needed.

3. Owner’s Pay Account. This account exists to pay you for the work you do in the business. It’s not tied to profits — it’s your salary or draw. That distinction is important.

4. Tax Account. Every time income hits, move a percentage of it into this account. It’s not optional. That money is already gone — it just hasn’t reached the IRS yet.

5. Operating Expenses (OpEx) Account. The OpEx account you actually use to run the firm. Rent, payroll, software, CLEs — everything gets paid from here. And only from here.

Sample Allocation Percentages to Get Started

Here’s one way to divide each deposit as it hits your Income Account:

| Profit | Owner Pay | Tax | OpEx |

| 5% | 35% | 10% | 50% |

Those numbers aren’t fixed. You’ll adjust over time as you track what your firm can realistically support. But starting small — especially with profit — builds the Profit First habit. Even setting aside 1% builds momentum and shows that your firm exists to create value, not just to pay bills.

Implementing Profit First Without Disrupting Your Entire Practice

Starting this system doesn’t mean reworking your entire billing process or accounting setup. Here’s how to begin without blowing everything up.

Open the bank accounts and watch the flow. Start by opening at least three accounts: 1) Profit, 2) Owner’s Pay and 3) Operating Expenses. Add the Tax account when you’re ready. Use your current bank or, if you wish, use a second bank to create some distance between the firm’s main operating funds and the cash you’re protecting.

Make allocations twice a month. Pick two days each month (e.g., the 10th and 25th) and make transfers based on whatever has landed in the income account. Don’t overthink the timing. Just make it consistent.

Run the firm from the OpEx account only. Running things from OpEx is what keeps the system honest. If there’s not enough money in that account to cover something, that’s a signal — not a reason to pull from profit or tax reserves.

What This Reveals About Your Pricing and Spending

Once you see how little ends up in the OpEx account after setting aside profit, tax and pay, you’ll start asking sharper questions:

- Are your fees actually covering the cost of delivering the work, or do you need to raise them?

- Are you spending on services or software you no longer need?

- Is your staff sized for your current case volume or your imagined future firm?

Profit-First accounting doesn’t just clean up cash flow. It exposes whether the way you’re handling money actually works. That’s a good thing!

A Quick Word About Trust Accounts

Profit First doesn’t change how you handle client trust funds or retainers. Any money not yet earned should stay in trust until it’s earned, then transferred to the income account before allocation. The same allocation rules apply once the funds become revenue. The key is to only apply the system to your earned income, not the money you’re holding on behalf of clients.

Don’t Let Profit Be a Dirty Word

In business and law practice, there’s an unspoken pride in sacrifice. Long hours, underpaid founders, reinvesting every dollar back into the practice — it’s all too familiar. But there’s nothing noble about running a practice that barely supports you. Profit isn’t selfish. It’s what allows you to:

- Pay your team on time.

- Invest in better tools.

- Serve clients without desperation.

- Sleep better at night.

Profit First gives you the structure to do all of that with less stress and more control. Personal injury attorney Adam Loewy adds: “If your firm isn’t financially stable, it becomes harder to focus on what really matters — serving your clients well and building a great team. Profit is what keeps the engine running strong. It’s not just support — it’s what makes long-term impact and consistent results possible.”

A Few Pitfalls and How to Avoid Them

The Profit First system is simple, but there are a few ways it can go sideways:

Skipping the bank accounts. You can’t just simulate this on a spreadsheet. The whole point is behavioral. Moving money between real accounts creates friction, in a good way.

Setting unrealistic percentages. Start small. Don’t try to jump to 20% profit immediately. Build your “profit muscle” over time and scale up as your firm adjusts.

Borrowing from the profit or tax accounts. This defeats the purpose. If the OpEx account is short, treat that as a sign you need to cut costs, not raid the reserves.

Expecting immediate results. Give it at least a quarter. You’ll feel the benefits faster than you think, but consistency matters more than early perfection.

What Changes When You Prioritize Profit

After a few months, the pressure around spending starts to ease. You stop second-guessing whether you can afford to pay yourself because the money’s already there. The profit account builds. Tax season stops catching you off guard. The firm feels steadier, and your decisions get sharper.

Most importantly, you start to feel like your law firm is working for you, not the other way around.

And that’s the whole point.

More Money Management Tips for Law Firm Owners

Law Firm Overhead: What It Is — and What It Isn’t

Are Your Law Firm’s Financial Systems Ready to Scale?

Law Firm Profits: 5 Ways You May Be Sabotaging Your Firm’s Growth

Image © iStockPhoto.com.

Sign up for Attorney at Work’s daily practice tips newsletter here and subscribe to our podcast, Attorney at Work Today.